The beginning of a new reorganization? Shinkin Banks in Tokyo start to move February 19th 16:21

On the 13th of this month, it was revealed that merger negotiations among Shinkin banks were taking place in Tokyo. Two credit unions with head offices in Adachi Ward and Katsushika Ward are proceeding with discussions.

If realized, this would be the first merger of Shinkin banks in Tokyo in 19 years. In Tokyo, where demand for funds is higher than in regional areas and the population is increasing, we looked into why reorganization is being undertaken now.

(Economics Department reporters Kentaro Makata and Mitsunori Saito)

Shinkin bank merger negotiations in Tokyo

Footwear store owner

: ``I was surprised to hear the news of the merger because I have been connected to this credit union since my grandparents' time.I hope that it will continue to be a kind and local-based credit union.''

The day after the merger negotiations were revealed, the owner of a footwear store in his 50s said this in a traditional shopping district in front of Shin-Koiwa Station.

The road in front of you is named ``Higashiei Shinkin Dori.''

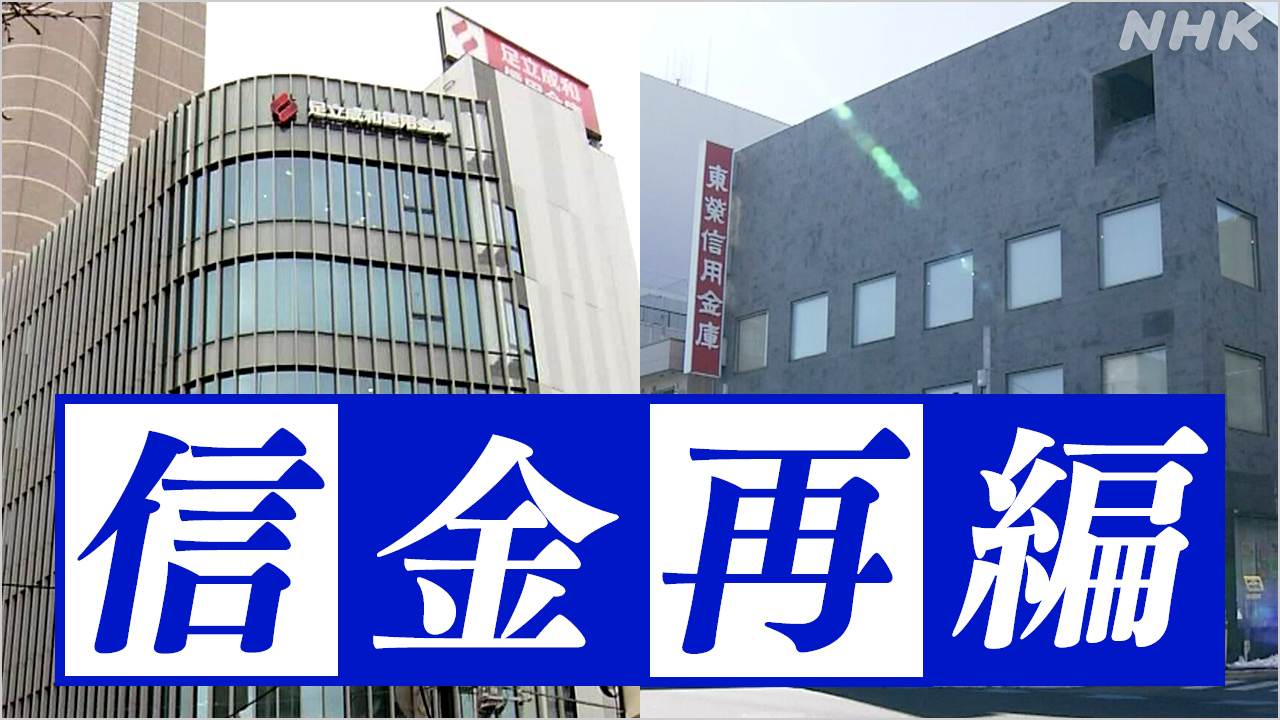

It is clear that this Shinkin Bank, whose head office is located about a 5-minute walk from the shopping district, is deeply rooted in the local area.

Toei Shinkin was established in 1933 and has 144 employees.

It operates 10 branches, mainly in Katsushika Ward, and has a deposit balance of 143.7 billion yen, the smallest of the 23 Shinkin Banks in Tokyo (as of the end of March last year).

He also visited the head office of Adachi Seiwa Shinkin Bank, the partner in the merger negotiations.

It is located in a shopping district near Kitasenju Station, which has prospered as a post town since the Edo period.

It was established in 1920 and will celebrate its 100th anniversary next year.

It has 433 employees, operates 23 stores mainly in the ward, and has a deposit balance of 577.8 billion yen, making it the 16th largest company in Tokyo.

A man in his 60s who runs a fruit and vegetable store near the main store said, ``He treats people with compassion and is willing to give advice.Even if there is a merger, I would like them to treat me with respect for the local area.''

This fruit and vegetable store originally had a relationship with a major financial institution, but they started doing business with a Shinkin Bank after they asked for some kind advice.

In front of the store's poster with a family photo printed on it, he said happily, ``Nariwa Adachi took the photo for me.''

If the merger goes through next year, it will be the first time in about 19 years since three Shinkin Banks in Tokyo became the Tama Shinkin Bank in 2006.

The total amount of deposits is approximately 720 billion yen, making it the 13th largest Shinkin Bank in Tokyo.

According to Tokyo Shoko Research, there are a total of 1,365 companies in Tokyo that use one of these banks as their main bank.

Although it is not on par with major banks or regional banks, it is expected to be the 18th financial institution out of more than 300 in Tokyo in terms of this number.

Why Tokyo?

Shinkin banks and regional banks have been taking the lead in merging and integrating in regions where population decline and declining birthrates and aging populations are becoming more serious.

On the other hand, this time the stage is Tokyo.

Behind this is a strong sense of crisis for the future.

If Tokyo enters a phase of population decline, there are concerns that the amount of deposits and loan profits will decline.

Before such a situation arises, we will strengthen our business foundation through a merger.

A person involved revealed the aim of the negotiations as follows.

Regarding Shinkin Banks, there has been a movement of people transferring their deposits to other financial institutions due to reasons such as inheritance.

Some point out that the number of customers, especially among the younger generation, is decreasing due to delays in digitalization.

Indeed, a store owner in a shopping district in Katsushika Ward who visited said, ``Many of my acquaintances used to work with Shinkin Banks, but it seems that number is decreasing now.''

Furthermore, there are concerns that if the expansion of NISA, a preferential tax system for individual investors, accelerates the movement of funds into stocks and other assets, the outflow of deposits will increase.

In fact, according to a summary by Shinkin Chukin Bank, the central organization of Shinkin Banks, the amount of deposits at Shinkin Banks as a whole continued to increase over the 20 years up to last fiscal year (FY2022), but as of September this year (FY2023). It is said that there are some credit unions in Tokyo whose deposit volume has started to decline compared to the same period last year.

There are still concerns.

There are growing expectations that the Bank of Japan will change its monetary easing policy.

Once the ``world of interest rates'' arrives in earnest, lending profits are expected to improve, but this time there is a possibility that interest rate competition for deposits with strong financial institutions will intensify.

Even in Tokyo, where the population is increasing, waves of change continue to wash over us.

It is believed that the two Shinkin Banks came up with this merger negotiation as a response to this situation.

Will the reorganization movement accelerate?

In response to this move, voices from the financial industry have been heard saying, ``Everyone is facing the same challenges.I think more shinkin banks will consider mergers.''

Will this spread to other areas in Tokyo and the 250 or so credit unions nationwide as expected?

The roots of ``Shinkin Banks'' lie in ``Credit Unions,'' which were created during the Meiji period to provide mutual aid to economically disadvantaged farmers, merchants, and businesses.

It is positioned as a non-profit organization, different from banks, which seek profits.

In principle, it is not possible for banks to cross borders and open branches in large cities and generate profits like regional banks.

That is why we have increased our presence through close relationships with individual stores and small and medium-sized enterprises.

This historical background and emphasis on local areas are also reflected in the picture the two Shinkin Banks envision after their merger.

As for stores, rather than simply merging or closing them, the company is expected to start reviewing their functions in line with the times, including advances in digitalization.

The government will also strengthen support for businesses through measures such as reassignment of staff.

We aim to be actively involved in issues faced by individual business owners and small and medium-sized enterprises, such as training successors and launching new businesses.

How will shinkin banks continue to demonstrate their significance as community-based financial infrastructure?

I would like to continue reporting on the trends of Shinkin banks, which are facing a difficult environment.

(Broadcast on “Good Morning Japan” on February 14th)

Economic Affairs Department reporter

Kentaro Makata Joined the Bureau

in 2011

After working in the Hiroshima Bureau, he covered the financial field at the Economic Affairs Department.

Economic Affairs Department reporter

Mitsutsune Saito

Joined the Bureau of Economic Affairs in

2017 After working in the Department of Economics Department, he covered the financial field.